How to calculate tax late payment interest and cases to apply

- 04/11/2021 17:53

✨ Organizations and individuals that are taxpayers are obliged to declare and pay tax on time, if the payment is late, you will have to pay extra money for late payment of tax, except for force majeure cases. Here are some contents about the cases of late payment of tax and how to calculate the late payment of tax, invite businessmen, organizations, individuals, and readers for reference!

1. 7 cases of late payment of tax

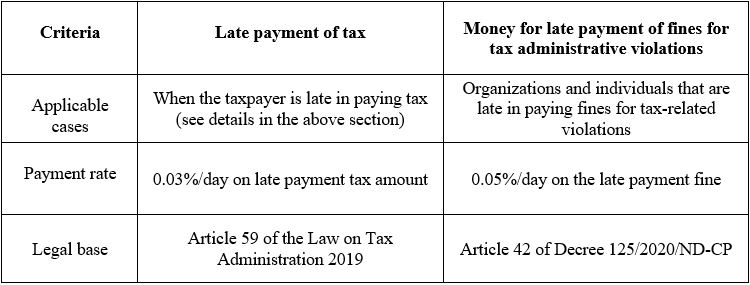

🍂 Clause 1, Article 59 of the Law on Tax Administration 2019 stipulates cases in which late payment interest is required, including:

- The taxpayer pays tax behind deadline, the extended deadline, the deadline written in the tax authority’s notice, tax liability imposition decision or handling decision;

- If the supplementation of the tax declaration dossier leads to an increase in the amount of tax payable, or the tax authority or inspecting authority finds that tax is understated, late payment interest shall be charged on the increase in tax over the period from the day succeeding the initial deadline or the deadline for tax payment of the initial customs declaration;

- If the supplementation of the tax declaration dossier leads to a decrease in the amount of refundable tax, or the tax authority or inspecting authority finds that refundable tax is smaller than the refunded tax, late payment interest shall be charged on the excessively refunded tax, which has to be paid back to the state budget, over the period from the day on which tax is refunded;

- The cases in which outstanding debt may be paid by installments as prescribed in Clause 5 Article 124 of this Law;

- The cases in which administrative penalties are not imposed due to expiration of the time limit for penalty imposition but outstanding tax has to be collected as prescribed in Clause 3 Article 137 of this Law;

- The cases in which administrative penalties are not imposed specified in Clause 3 and Clause 4 Article 142 of this Law

- The organization that is authorized by the tax authority to collect tax but fails to transfer the tax, late payment interest and fines paid by taxpayers to the state budget in a timely manner shall pay interest on such amount.

2. How to calculate tax late payment interest

🍂 Clause 2, Article 59 of the Law on Tax Administration 2019 stipulates the rate of late payment tax and time for late payment interest as follows:

a) The rate of late payment interest is 0,03% per day on the overdue amount;

b) The period over which late payment interest is charged is a continuous period from the day succeeding the day on which late payment interest is charged as specified in Clause 1 of this Article to the day preceding the date of payment of the outstanding tax, refunded tax, increase in tax, imposed tax, late payment tax has been paid into the state budget

Thus, the one-day late payment interest is calculated as follows:

1 day late payment amount = 0.03% x Tax amount for late payment

3. When is late payment interest exempt?

🍂 According to Clause 8, Article 59 of the Law on Tax Administration 2019, in principle, taxpayers must pay late payment interest but will be exempted from late payment interest if they fall into force majeure circumstances, specifically:

- Taxpayers suffer material damage due to natural disasters, epidemics, catastrophes, fires, unexpected accidents.

- Other force majeure cases according to the Government's regulations.

4. 4 cases that late payment interest is not charged

🍂 Clause 5 of the Law on Tax Administration 2019 stipulates cases in which no late payment interest is charged, specifically:

- The taxpayer provides goods/services which are covered by the state budget, including sub-contractors in the contract with the investor, and are directly paid for by the investor. If such goods/services are not yet to be paid for, late payment interest will not be charged.

- Goods subject to assessment and analysis to determine the exact amount of tax payable shall not be charged late payment interest while waiting for assessment and analysis results.

- Goods that do not have an official price at the time of customs declaration registration will not be charged late payment interest during the time when the official price is not available.

- Goods with actual payments, goods with adjustments added to the customs value that has not been determined at the time of customs declaration registration, are not required to pay late payment interest during the time when the amount has not been determined the actual payment, adjustments added to the customs value.

⚡ Note: Late payment interest has not been charged in cases where debt is frozen according to Article 83 of the Law on Tax Administration 2019.

5. Distinguishing late tax payments from late tax fines

📌 Tax-related late payment interest includes two types: late payment interest and late payment fines for tax administrative violations.

📌 Both are late payments, but these two types are different in nature and level of payment, specifically

✨ There are some regulations on late payment of tax specified in Law on Tax Administration No. 38 of 2019, if customers have any questions, please contact the TASCO Tax Agent via hotline: 0975.48. 08.68 (zalo) for direct advice!

TASCO - Tax agent responsible for all service

TASCO - Give trust - get value

Please contact TASCO for a free consultation:

Hotline: 086.486.2446 - 0975.08.68 (zalo)

Hotline: 086.486.2446 - 0975.08.68 (zalo)

Website: dailythuetasco.com hoặc dichvutuvandoanhnghiep.vn

Email: lienhe.dailythuetasco@gmail.com

Comment

main.comment_read_more